Non-performing loans on the rise

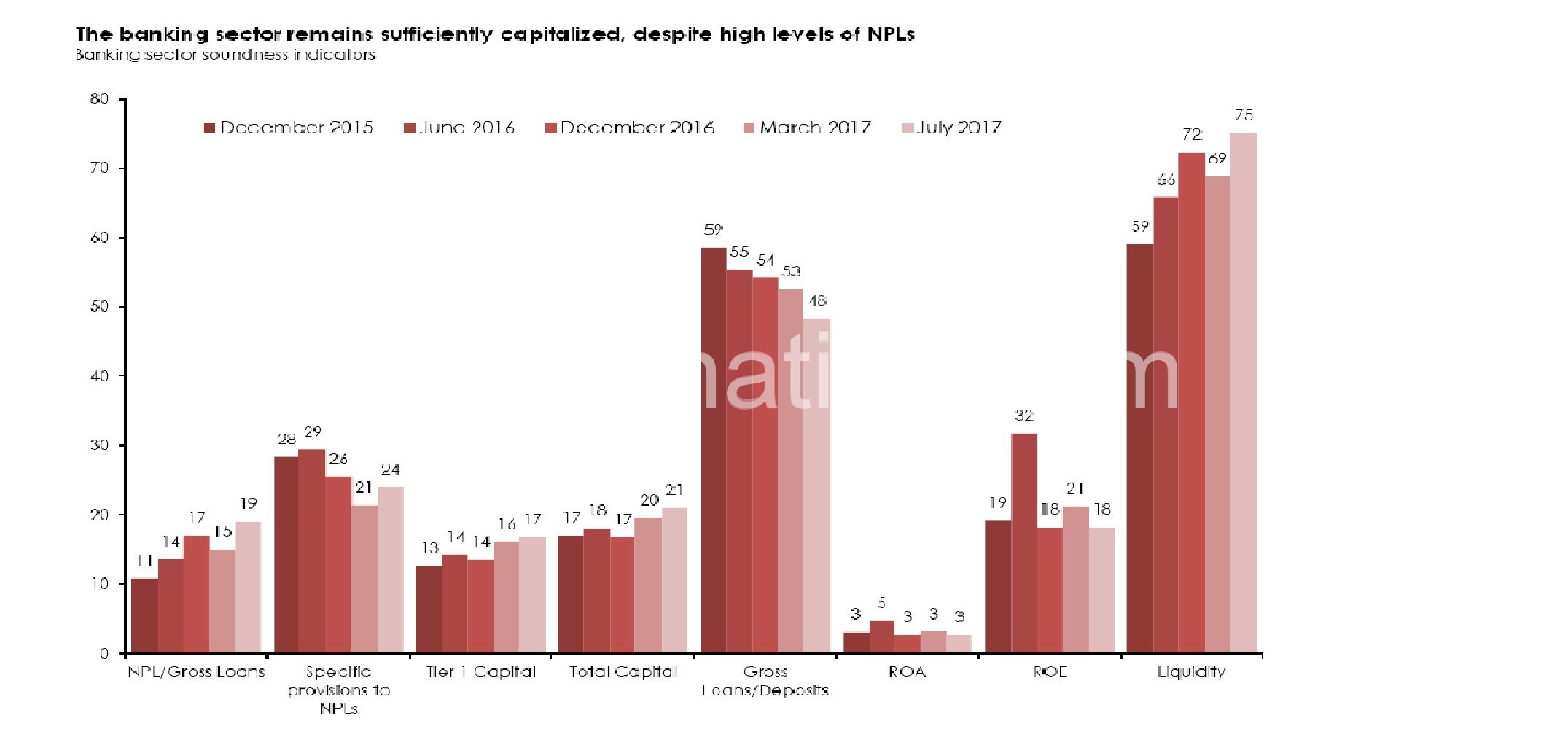

Malawi’s level of non-performing loans (NPL) has risen to above the regulatory benchmark of five percent, standing at 19 percent as at July 2017, from 10.8 percent in December 2015, World Bank statistics have shown.

According to the November 2017 Malawi Economic Monitor titled ‘Land for Inclusive Development’ published last week, the high NPL ratio is indicative of the difficult economic situation, with borrowers often failing to generate sufficient returns from their businesses to repay their loans.

The situation is exacerbated by Malawi’s high interest rates. The provisioning for NPL’s was on a declining trend up to mid-2017, when it started to reverse, as banks had to put aside extra funds to cover for potential loan losses.

“The situation is exacerbated by Malawi’s high interest rates. The provisioning for NPL’s was on a declining trend up to mid-2017, when it started to reverse, as banks had to put aside extra funds to cover for potential loan losses.

“This affected the banking sector’s overall level of profitability, as reflected by the decline in Return on Assets (ROA) and Return on Equity (ROE). Thus, the constraints facing the banking sector have resulted in an increase in liquidity and a decline in the ratio of loans to total deposits,” said the bank in the report.

According to the report, the low level of capitalisation of some banks and the increasing level of NPL’s continue to pose a significant threat to the financial stability of the banking sector.

In an earlier interview, Bankers Association of Malawi (BAM) chief executive officer Violette Santhe said NPL’s impact funding costs as they reduce interest earning assets with the attendant risk of write off reflected through provisions.

Economist Gilbert Kachamba however is on record as having said an increase in nonperforming loans, at 69 percent in 2016 or a ratio of 17 percent, is quite huge and worrisome for a small country like Malawi.

“This impacts the economy negatively especially the financial sector. The NPL’s bring stress in the economy as the financial sector is faced an array of risks like liquidity risks, market risks and operational risks.

“Now with the reduction in interest rates, banks must respond accordingly and favourably to this reduction and we expect NPL’s to fall. Banks should also intensify in client screening to make sure that those who are accessing the loans have the ability to pay back,” he said.

According to the report, Tier 1 capital increased slightly from 16.1 percent in March 2017 to 16.8 percent in July 2017, while the total capital to asset ratios increased from 19.5 percent in March 2017 to 21.0 percent in July 2017.