Banks see less impact of policy rate cut

Bankers Association of Malawi (BAM) has said while the new policy rate will affect interest rate margins in the short-term, commercial banks remain positive on gains to be accrued from increased volumes and reduced credit losses.

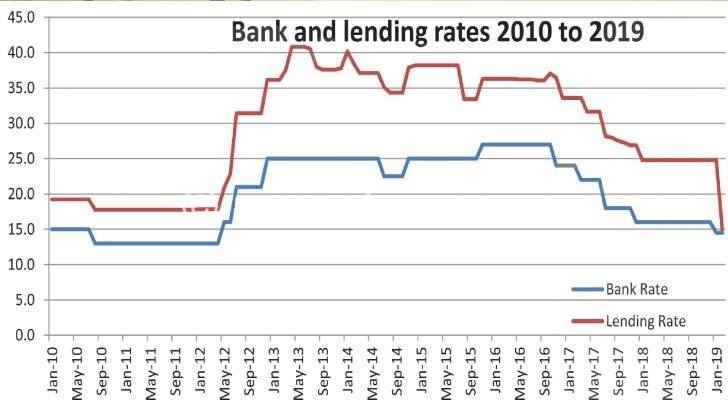

BAM’s sentiments are in reaction to last week’s Reserve Bank of Malawi (RBM) 100 basis points cut in the policy rate or bank rate from 14.5 percent to 13.5 percent, a move that is expected to provide relief to borrowers.

In a written response to questions yesterday, BAM chief executive officer Violette Santhe said while the new base lending rates will be determined by individual banks, there will be improved loan repayments following reduced lending rates.

“Each bank will review the new policy decision and depending on that assessment, it will develop response plans based on individual business.

“However, risk premiums are different for different classes of clients, obviously higher for small and medium enterprises [SMEs]. Banks are always seeking better ways to lend to this sector in line with its creditworthiness,” she said.

Santhe, however, said in addition to the conventional lending instruments, commercial banks have already started to collaborate with other stakeholders for innovative financing, which she said can support some pockets of SMEs not able to meet existing loan covenants in the banking industry.

“It is important to understand that compliance on banks’ risk management trend is increasing in the form of regulation and international standards such as Basel II and International Finance Reporting Standard 9.

Santhe said the Malawi economy needs to exploit innovative financing models to fill this gap by addressing specific market failures and institutional barriers.

She said for innovative financing to happen, there is need for collaboration among public, private and or philanthropic sources of finance.

“Innovative financing provides a set of tools for donors who want to create more development impact through their investments, private companies open to new business models in new markets and financial institutions looking for new opportunities,” she said.

Some of the possible innovative financing solutions in the agricultural SMEs include risk sharing facilities, loan portfolio guarantees, new product design, irrigation and water systems, post-harvest storage facilities and rural feeder roads.

Last week, the central bank cut key driver of interest rates on loans, the second since January this year.

In January, RBM also slashed the policy rate—the rate at which commercial banks borrow from the central bank as the lender of last resort—by 150 basis points from 16 percent to 14.5 percent, a move that saw commercial banks softening their lending rates to a minimum of 14.9 percent and a maximum of around 26 percent.

Chamber of Small and Medium Enterprises executive secretary James Chiutsi on Saturday said small businesses require long periods of incubation to reach required production capacities.

On his part, National Working Group on Trade and Policy chairperson Frederick Changaya said banks should be innovative by, among others, partnering SMEs and growing them into big players.

He observed that many commercial banks scramble for the same over-banked firms yet some of the start-ups or SMEs have better future potential than big companies.