Declining results for insurers: endangered species

Nearly all large insurance companies (based on total assets) posted nose-diving results in 2014, twisting the profitability graph to unpack a ‘peaks and troughs’ trend in so far as performance of local financial institutions entails, but the underlying fact is that all banks and insurers have at least registered profits for the first time since the profitability barometer aka profitrometer¹ incepted in 2012.

Nevertheless, this analysis, like the preceding and subsequent analyses, predominantly focuses on the financial performance of insurance companies operating locally.

Insurers have succumbed, on average, to unprecedented 17 percent decline in profits as compared to results in 2013. Aside from the regressive results, the profitability ranking in the top five – comprising NICO Life, Old Mutual, NICO General, General Alliance and Malawi Re, remained chronologically unchanged.

Unlike insurers in top five, the sixth ranked United General made a slight profit growth of K14 million but Prime is the most improved insurance company in the year under review having risen from the lowest bottom to the seventh position. In 2013, Prime posted a whopping K292 million losses, worse than the 2011 negative results of K238 million. However, the 2014 profits outclassed the 2012 margin by K129 million.

Other insurers with improved results include Reunion (8th), Charter (10th) and Smile Life, currently anchoring the table of twelve players. Unfortunately, the improvements these companies made were less influential to gain elevation to the club of “corporate billionaires”.

Though shareholders of Real (9th) were optimistically expectant of better results than achieved in 2013, the directors of this sole publicly listed insurance company have, in the mean time, something to write home about ahead of the release of the company’s half-yearly results after June 30 2015, given that the first quarter results are out.

Performance metrics for general insurers

The above analysis clearly vindicates the essence of considering bottom line² growth as one of the key performance indicators (KPIs). The other KPIs or performance metrics unique to general insurance business include combined ratio which can be decomposed into claims ratio and operating expenses ratio.

As defined by the Economic Times, combined operating ratio (COR) is …”the sum of incurred losses and operating expenses measured as a percentage of earned premiums”. Essentially, the COR measures the profitability of an insurer’s underwriting activities.

A combined ratio of less that 100 percent is considered better as it shows that the insurer is earning more by way of premiums relative to the claims paid and the operating expenses incurred.

According to the Reserve Bank of Malawi’s Financial Stability Report of 2013, the COR for the general insurance subsector was 64 percent in the third quarter but the best ever was achieved in the first quarter with 47 percent. Thus, the general insurance subsector made a 53 percent underwriting profit, probably, the best ever underwriting results recorded in recent years.

Globally, the resounding underwriting performance of Oxbridge Re, which provides reinsurance business solution primarily to the property and casualty insurers in the Gulf Coast region of the US, cannot be overlooked.

The combined ratio of Oxbridge Re in the first quarter of 2014 was 28.2 percent but it deteriorated in the first quarter of 2015 to 39.4 percent. The company incurred no insured losses in both quarters – quite rare.

Locally, based on 2014 consolidated annual accounts published in The Nation and The Daily Times, the general insurance subsector’s COR improved by one percent point as compared to 103 percent recorded in 2013.

Insurance is, arguably, a business of break-even results given the fluctuating trend which keeps evolving and causes unbearable distortions in data analyses and conclusions as justified in subsequent paragraphs.

The 2014 Financial Stability Report of RBM shows that the COR was 98.5 percent in September down from 100.1 percent in March 2014, averaging 99.3 percent.

Elsewhere in the US, the ‘property and casualty’ insurance which is the insurance business that excludes life and health policies, on average, broke even in the first half of 2014 – combined ratios for commercial and personal lines were 99 percent and 101 percent respectively, according to Swiss Re Global Insurance Review 2014 and Outlook 2015/16.

According to Aon Benfield, the global combined ratio was 99.1 percent in 2013 but the consistent vindication is Swiss Re’s forecast of 100 percent combined ratio for 2015.

The combined ratio over 100 percent is indicative of unprofitable underwriting activities but vindictive of the flipside of insurance (the business of taking risks of others).

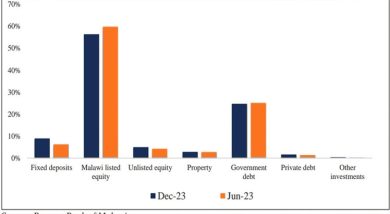

Beyond underwriting operations, insurers have the potential of making profits despite a COR over 100 percent as they rely on investment income. To this effect, most insurers attribute the dwindling results in 2014 to malign investment environment. Yet, some resilient insurers have produced positive investment returns in similar circumstances. Such resilience can be sustained, in the longer term, by a robust enterprise risk management (ERM) framework.

The situation remains equally volatile even for advanced economies. The US insurance industry has recently underperformed owing to low interest rates offered in the capital markets. The UK

Financial Stability Report of December 2014 confirms that …”Governments bond yields across many advanced economies (including the UK) continued on the downward trend…”

One line item on the balance sheet that deserves special attention is reserves. Most insurers across the globe utilise prior year claims reserves to recoup poor underwriting results. According to the US-based Insurance Information Institute, the US insurance industry reported releases of prior year reserves totaling $5.5 billion for the first quarter of 2014. A record high reserves release was also noted in the UK.

As motivational as it seems, nevertheless, the UK prudential regulator, the Prudential Regulatory Authority (PRA) cautioned the British insurers to desist from such ostensible ‘bad practice’ although Deloitte had predicted that the UK motor insurance would make underwriting losses of up to £1 billion in 2009 without the support of prior year releases.

In a recent letter addressed to the insurance chief executives, the PRA warned that, “…the PRA will question the robustness of the underwriting practices at firm that unduly rely on prior year reserves releases to support ongoing underwriting activity for any substantial period of time.”

The PRA argue that some insurers had been tempted to weaken their underwriting selection criteria to protect their market position and that in doing so may endanger their ability to meet policyholders’ future claims in the event of reserves depletion.

The study that the Insurance Times carried out on six UK-domiciled insurers (Direct Line, RSA, Aviva, Allianz, Ageas and AXA) based on ‘2013 PRA returns’ revealed that the collective combined ratio of these insurers was 100.3 percent when in actual sense it would have deteriorated to as far as 110.7 percent without reserve releases.

Reinsurers are not seamless either. For example, Swiss Re, one of the largest global reinsurers acknowledged that the profitable results which the reinsurers produce are actually a product of underwriting activities, investment income and worst of all, prior year claims reserve releases. It challenged in its recent report that without the prior year reserves release, reinsurers would likely make huge losses.

One can be tempted to conclude that universally the insurance industry produces recycled underwriting profits as the premium income generated in one financial year is rebooked in subsequent calendar years. The concerns of PRA are valid.

Loss ratio is the percentage of net earned premium (NEP) that insurers pay out in claims. A benign claims environment fixes the loss ratio at 60 percent or below, the benchmark within which the non-life insurance sector achieved in 2014 – precisely, 55 percent. Conversely, it is projected to surge to a minimum of 70 percent in the wake of 2015 flash floods.

A moderate deterioration of claims loss ratio is attributable to the country’s very low penetration ratio. Likewise, insurers in Nepal (in the aftermath of the recent tragic earthquake) have escaped the worst and costly claims environment in decades for the same reason of low penetration ratio.

When loss ratio strikes 100 percent, it does not imply a break-even point, rather two different things. It is either the insurers are not properly managing claims costs (in the context of insurance fraud, outsourcing and claims inflation) or else the policyholders are making genuine claims and, therefore, reaping from where they had sowed and enjoy the fruits of their generosity for allowing insurers to invest the premium income they had paid prior to the occurrence of the insured events.

Approximately 31 percent of NEP accounted for management expenses. The non-life sector also incurred 16 percent of NEP in acquisition costs, resulting in the operating expense ratio of 102 percent, as highlighted above.

On global scale, insurers are ranked based on an insurer’s premium revenue criteria and the top ten insurers account for over $1 trillion in total revenue. According to the Insurance Information Institute 2013 data, the top five insurers comprise Berkshire Hathaway (US), AXA (France), Japan Post Holdings, United Health Group (US) and Allianz (Germany). Using assets-based ranking criterion, AXA leads with over $1 trillion in total assets followed by Allianz ($983 billion).

In 2014, the local non-life insurance subsector generated K34.6 billion in gross written premium (GWP) against prior year premium revenue of K26.6 billion, representing a 30 percent top line growth for the subsector.

About 26 percent of the total GWP was ceded to reinsurers, inferring that the general insurance sector retained almost three-quarters of the total premium written in 2014, two percent points more than outward reinsurance cost the subsector incurred in 2013, but approximately 5 percent points

lower than recorded in the last quarter of 2014, according to RBM’s September 2014 financial stability statistics.

However, life insurance companies are not only risk takers but also risk retainers, consuming reinsurance products with just less than 10 percent of their premium revenues in many years. Perhaps, this is the reason this subsector incurs huge losses, which adversely impact on profitability year-on-year.

Highly performing banks

The banking sector continues to over perform. National Bank’s bottom line growth has quadrupled just in four years since 2011 when it was anticipated that the company’s profits would plateau at K12 billion plus, as the case with Standard Bank. Finally, the neck-to-neck profitability tie the two giants of the financial services industry had in the past three years has come to an abrupt end, either for a while or forever.

Above everything else, FDH Bank deserves congratulations on ascending to the top four banks, pushing NBS Bank to the fifth position of corporate billionaires measured by marginal returns.

FDH Bank is on record to become the swiftest financial institution to publish its annual accounts in the public domain within 42 days from the fourth quarter balance sheet date.

The fiscal year for financial institutions tentatively ends on December 31 – FDH had its accounts published in The Daily Times of February 11 2015 (and The Nation newspaper dated February 13 2015), beating the statutory deadline of April 30 by 78 days.

Certainly, FDH Bank’s early publication of its accounts was influenced by the motivation of resounding performance. Standard Bank did the same last year.

Assuming all financial institutions or specific sectors or subsectors can, by compulsion, publish their financial statements in the said newspapers on the same date, will it make any difference at all in terms of profitability levels? This controversial assumption is open for debate.

Ecobank Malawi takes the sixth position contrary to the company’s claims in The Nation newspaper of March 27, 2015 that it qualifies to the top five of highly profitable banking institutions.

Malawi Savings Bank (MSB), which is currently immersed in financial and political turbulence waters, is the only financial institution without latest publicly published financial statements extracts, in contravention of Section 37(2) of the Financial Services Act 2010. However, MSB reported K500 million profit with 150 percent profit growth in 2013.