Market analysts assess impact of devaluation

Market analysts say the 25 percent devaluation of the kwacha effected on May 27 has not improved foreign exchange liquidity challenges and the exchange rate.

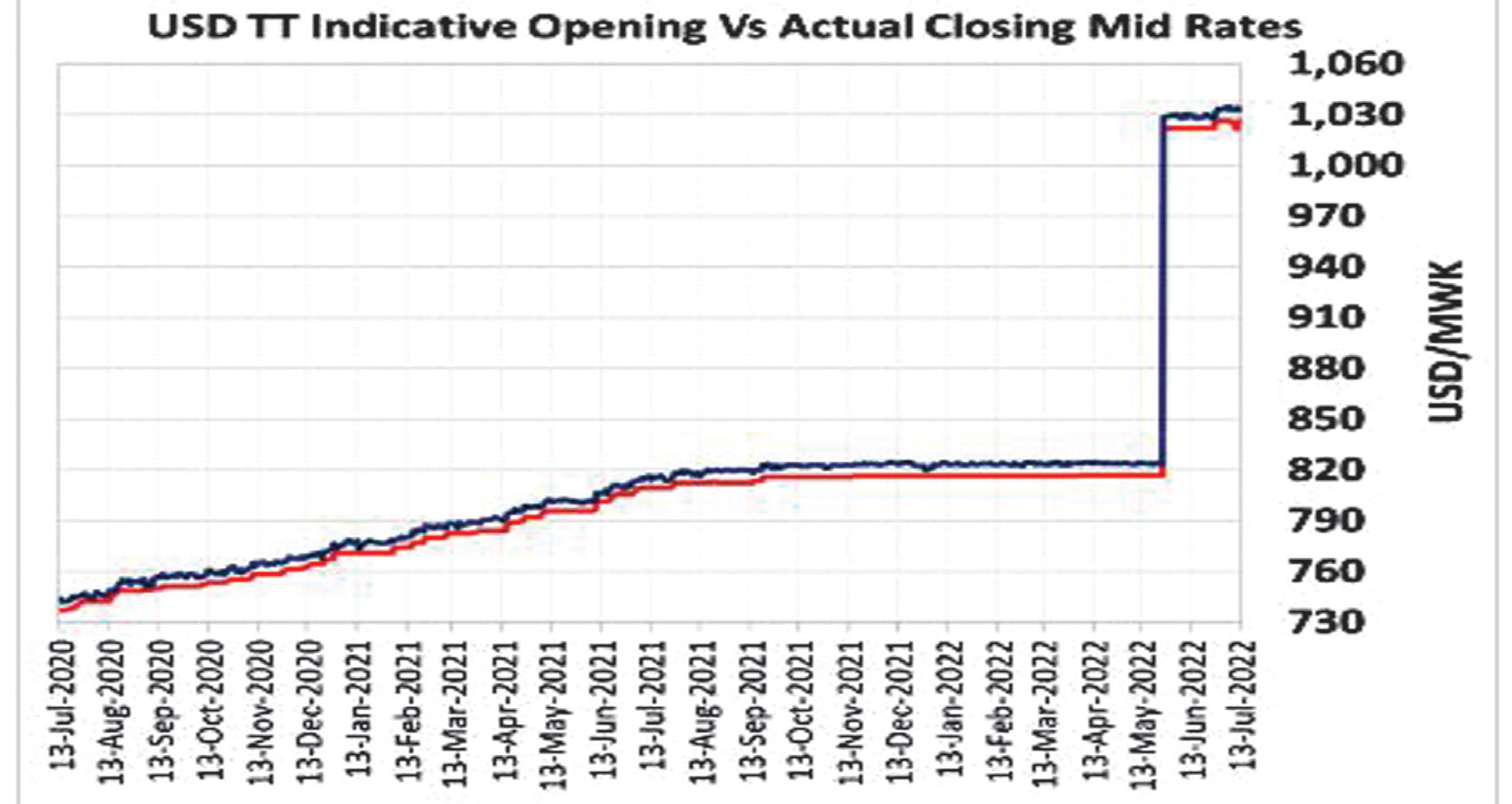

The analysts said this in separate interviews yesterday against the background of the devaluation of the kwacha, which Reserve Bank of Malawi (RBM) Governor Wilson Banda argued was necessary to align the foreign exchange supply to the macroeconomic fundamentals and ensure supply of foreign exchange in the formal market.

Speaking in an interview, Financial Market Dealers Association of Malawi (Fimda) president Maclewen Sikwese said devaluation has failed to achieve some key objectives.

He said: “On ensuring alignment between the Authorised Dealer Banks [ADBs] telegraph transfer [TT] rates and cash bureau rates to create a unified market clearing exchange rate, a quick look at the ruling bureau cash rates and the ADBs TT rates does point to widening spread between the two market rates after a brief period of alignment.”

Sikwese said despite a more accelerated pace in the widening of the spread, the general direction was expected as the two markets differ in both depth and the variables that affect the pricing of the foreign exchange.

He said unlocking flows from hoarders, the market has seen an increase in inflows with the average of $6.3 million (about K6.4 billion) traded per day post devaluation from $4.8 million (K4.9 billion) in May before devaluation. He said this could be as a result of tobacco inflows.

Market analyst Bond Mtembezeka said devaluation of the currency has not done Malawi any good largely because the country is a net importer.

He said: “Devaluation is done to align a local currency with foreign currencies when the former can no longer be supported owing to persistent current account imbalances.

“The rationale is that once a currency is devalued, on one hand an economy’s exports become competitive on the global market, therefore, the economy exports more and on the other hand, its imports become expensive, thereby dissuading economic agents from importing more.”

But Mtembezeka said in Malawi’s case, the economy is still importing more and at the same time the export base is narrow and undermined by supply side bottlenecks.

Catholic University economics lecturer Hopkins Kawaye said it is too early to examine the full impact of the devaluation, but said the growth of the reserves by the end of this month will give a true picture of the impact.

Lately, Malawi has faced foreign exchange shortages with data showing that gross official reserves under the direct control of the central bank stood at $388.22 million as at May 31 2022 from $443.25 million during the same period last year.

The drop in the reserves, according to market analysts, reflects the increasing burden on RBM to support the foreign exchange market with liquidity to smoothen the rate of depreciation.

In a paper titled ‘Is Devaluation an Option for Malawi’s Current Debt Challenge’, economists Thomas Chataghalala Munthali and Frank Ngalande warned that devaluation should not be an option as it would cause more harm than good.

“The only case for justifying devaluation in Malawi is simply making efforts to bring more of the forex into the official avenues so that those with forex should be encouraged to sell to official dealers,” they said.