The Reserve Bank of Malawi (RBM) has outlined measures to improve pension remittances, including facilitating payment plans for employers.

The measures, outlined in an e-mailed response to our questionnaire, strike a delicate balance of forcing the eggs (pensions) out of struggling employers to pension fund managers without choking off the very goose (employers) that lay the eggs.

RBM spokesperson Mark Lungu said, among other measures, the central bank has been engaging non-compliant employers, and “requiring them to commit to a payment plan through legally enforceable undertakings”.

The need for RBM—which also doubles as the registrar of financial institutions—to manage competing interests of employers on one hand and employees on the other comes out clear in separate interviews with representatives of both sides.

Employers Consultative Association of Malawi (Ecam) executive director George Khaki said RBM’s engagement strategy is the best route as it protects both employers and employees in an environment where organisations are struggling with liquidity.

Khaki said employers are finding it hard to balance revenue and expenditure, but whenever revenues improve, they are prioritising paying current pension obligations even as they also cater for pension arrears.

“In the meanwhile, if any pension payment is due, companies scrounge for resources to pay off the maturing pension dues.However, the strategies that are being used depend on the circumstances each company is facing and what their priorities are,” he said.

Khaki said employers recognise that not remitting pensions is unfair to employees; hence, by engaging the employers at an individual level, RBM will assess the challenges that the employers are facing and identify solutions tailored to the employers’ needs.

But Malawi Congress of Trade Unions (MCTU) secretary general MadalitsoNjolomole, while supporting dialogue, urged RBM to follow the letter of the law and enforce all applicable laws to ensure that employers remit their pensions.

He said: “Engaging the employers is good. But RBM should stop being lenient with the employers.”

RBM has in recent times expressed concerns over pension contribution arrears and vowed to address non- compliance and bring sanity to the pension industry.

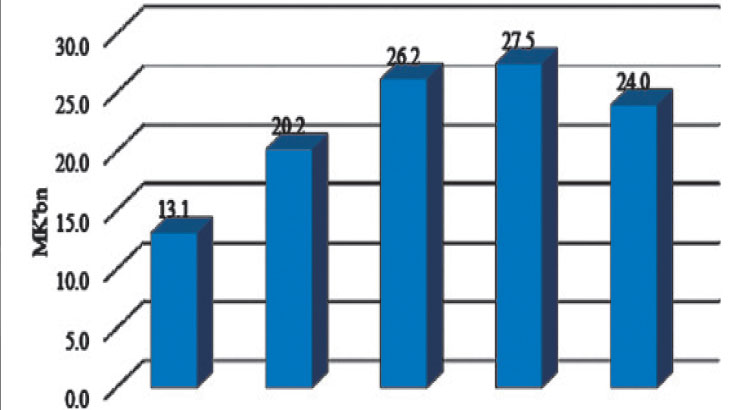

As of June this year, unpaid pension arrears peaked at K31.1 billion, up from K23 billion reported in December 2022, according to RBM data.

During the period, there were 894 employers who defaulted, accounting for 24.1 percent of the total number of employers participating in the National Pension Scheme.

Furthermore, consumer complaints against the pensions sector continue to rise, claiming the highest number of cases lodged to the registrar of financial institutions, figures show.

According to the RBM analysis, the pensions sector took up 43 percent of all the complaints in the financial sector.

While indicating that the majority of employers are in compliance with the Pension Act, Lungu noted that the National Pension Scheme is mandatory; hence, all employers are expected to comply.

He said: “The Registrar [RBM governor] is now issuing monetary penalties to penalize non-compliant employers, freezing assets of employers who continue to be non-compliant with the Act and physically closing the premises of non-compliant employers to enforce compliance.”

According to Lungu, the Registrar of Financial Institutions has also, among others, been conducting pension awareness campaigns to inform both employers and employees of their rights and obligations under the Act.

To address the issue of non-placement on pension by employers, Lungu said the registrar is currently in the process of establishing a comprehensive database of employers in the country.

The database, according to Lungu, will serve multiple purposes, including the identification of employers who have not yet implemented pension schemes for their employees and facilitate the issuance of certificates of compliance to employers who require them.

“For instance, in certain situations, employers may need to obtain a certificate of pension compliance to secure contracts. This requirement is particularly common among employers who prioritise social rights and choose to collaborate only with companies that provide pension benefits to their employees,” he said.