The spread between the official and market parallel exchange rates has widened by about 42 percent as foreign exchange reserves continue to drop, putting pressure on the kwacha, it has been established.

Money market analysts have since attributed this situation to an overvalued exchange rate despite the 25 percent devaluation of the kwacha effected on May 27 this year.

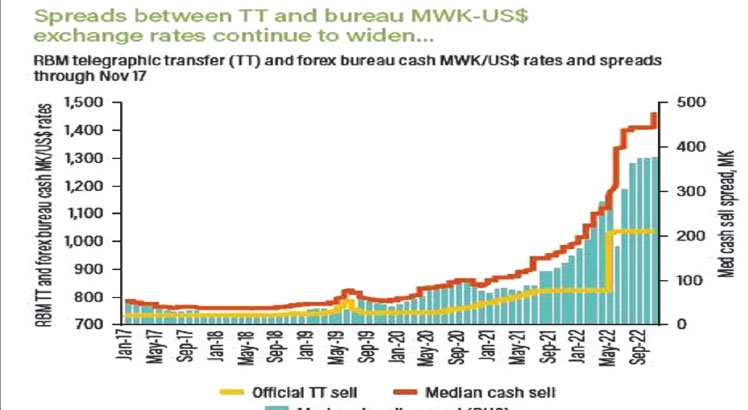

Reserve Bank of Malawi (RBM) data based on World Bank calculations shows that between July 2021 and May 2022, the official kwacha exchange rate for telegraphic transfers (TT), through which most foreign exchange transactions are conducted, marginally depreciated by 1.4 percent.

On the other hand, foreign exchange bureau cash exchange rates depreciated by 25.6 percent, widening the spread against the TT rate by 42 percent.

The data further shows that as at November 17, the official TT selling price was at around K1 030 while cash selling price was at around K1 450 against the dollar.

Speaking in an interview yesterday, money market analyst Cosmas Chigwe said that at 42 percent, the spread between the official TT rates and cash rates implies that devaluation of the local unit has not brought the desired impact.

He said: “Usually, the cash rate tends to trade much closer to the parallel market rates and the widening of the spread is simply indicative of an increasing supply and demand imbalance.

“This suggests that despite the devaluation, the central bank continues to maintain overvalued exchange rates while unable to ensure that supply of foreign exchange meets legitimate demand transactions at that price.”

In his reaction, money market analyst Bond Mtembezeka said while the widening spread was expected, devaluation of the kwacha does not help net-import economies such as Malawi.

He said ideally, devaluation was supposed to first dissuade economic agents from importing, but also make the country’s exports competitive.

Said Mtembezeka: “The two forces are, therefore, supposed to work towards improving the current account and bring about a sustainable equilibrium.

“However, you have to understand that Malawi is a net importer and we import practically everything, which means devaluation does not have positive effects.”

To align official rates with market rates and address foreign exchange shortages, RBM on May 27 this year devalued the kwacha by 25 percent.

At the time of the devaluation, RBM Governor Wilson Banda said the move was necessary to align the foreign exchange supply to the macroeconomic fundamentals and ensure supply of forex in the formal market.

While imports and other international foreign exchange transactions have declined, RBM data shows that foreign exchange reserves remain low, largely caused by a structural trade deficit and rising debt-servicing payments to external commercial creditors.

Meanwhile, gross official forex reserves have decreased by more than half from $847 million (about K877 billion) in December 2019 to $326 million (about K338 billion) in October 2022, or about 1.3 months of import cover.

This is much lower than the recommended 3.9 months of import coverage for a credit-constrained economy such as Malawi, according to International Monetary Fund statistics.

The declining foreign exchange reserves increases the burden on RBM to support the foreign exchange market with liquidity, according to analysts.