Businesses are expected to experience a reduction in availability of loans as most banks plan to tighten credit standards and conditions up to June 2024.

The reduction in the availability of loans is largely due to the expectations of a continued unstable macroeconomic environment resulting from rising inflation and the acute foreign exchange shortage.

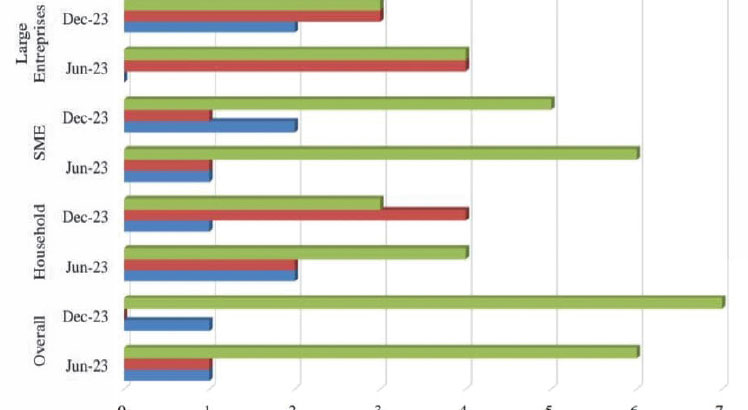

However, banks expect credit standards and conditions for households to ease mainly attributed to the access of payroll loans, which are deducted at source and reduce the risk of default, a bank lending survey shows.

The tightening of the lending conditions is happening at a time the stability of the banking sector has registered a marginal decline, falling to 0.68 in December 2023 from 0.75 in June 2023 because of the decrease in the capital adequacy, liquidity and profitability of the banking system, according to the survey.

It also coincides with increasing demand for loans and rising non-performing loans or bad debts in the sector.

Speaking in an interview on Tuesday, investment banker Misheck Esau argued that the type of credit that should be tightened is consumption lending as deficit spenders drive so many fundamentals, including inflation and balance of payments position to the gutter.

He said: “What the financial sector should be doing for businesses that are in production is to make credit cheap and more accessible.

“Majority of the Malawi economy is largely informal and this kind of approach punishes the few that have access to credit and continues to exclude those that are outside the formal finance net.”

Esau said this is partly the reason the economy is not ticking and the country continues to export jobs through imports.

Market analyst Cosmas Chigwe said in an inteview on Tuesday that while tightening credit conditions can be a prudent measure to mitigate risks for banks in the short-term, the measure could exacerbate financial pressures on businesses, potentially leading to reduced investments, slower growth and business closures.

He said: “There is a school of thought that feels banks have just become relatively lazier, owing to the ever-present demand for financing by government and government agencies.

“This provides enough of an investment avenue for banks to make money without having to go through the hassle of private credit assessments.”

Chigwe said the strategy could spell further reduction in private credit extension by banks with “unfortunate consequences”.

He said banks should, instead, focus on refining their lending strategies to ensure more involvement in the businesses they are lending to, investing more in improving monitoring and governance of the businesses rather than just staying away entirely.

Economist Bond Mtembezeka said while a deteriorating macroeconomic environment heightens credit risk, leaving banks with no option to tighten credit could help curtail bad loans.

“Now the measure becomes convenient at this point when government securities which are less risky are an attractive investment presently,” he said.

Chamber for Small and Medium Businesses Association executive secretary James Chiutsi said the approach shows the “little regard” banks give small and medium enterprises.

He said: “It is predatory. We expected the lending institutions to stand with us, not abandoning us. This is the time that we need them. By tightening the noose, it simply means they don’t care what happens to us

“We believe that government gives a lot of business to the banks, such that, SMEs business means little to them.”

Meanwhile, Reserve Bank of Malawi (RBM)figures shows that credit to the private sector from commercial banks rose from K1.07 billion to K1.21 billion during the second half of 2023.

During the same period, annual private sector credit growth decelerated to 17.9 percent in December 2023 from 24.1 percent in December 2022.

In real terms, the annual growth rate in private sector credit remained negative and stood at minus 11.3 pecent in December 2023 from minus 1.3 percent in December 2022, according to RBM figures.

Ironically, the banking sector’s non-performing loans (NPLs) ratio improved to 6.1 percent from the 6.9 percent registered in June 2023.

This is, however, above the tolerable limit of five percent, with most banks anticipating defaults on all economic agents to increase in the forecast period of January to June 2024 due to banks’ expectations on the effects of the foreign exchange shortage and local currency realignment, rising inflation, rising interest rates, high public debt and tight fiscal policy.

The NPLs were concentrated in four sectors, namely wholesale and retail trade, restaurants and hotels, community, social and personal services and agriculture, forestry, fishing and hunting,

In the December 2023 Financial Stability Report, RBM Governor Wilson Banda said the resilience of the domestic financial system will be sustained over the half-year to June 2024 forecast period.