Malawi’s foreign exchange market reforms are said to show early signs of progress, but experts say the external sector remains under strain as forex shortages persist and international reserves stay well below comfortable levels.

Data contained in the Afreximbank African Trade Report 2026 shows that foreign exchange reserves growth improved from minus 29 percent in 2021 to 0.9 percent in 2025, but gross international reserves still declined from about $400 million (about K700 billion) to $200 million (about K350 billion) while import cover dropped from 1.4 months to below one month, way below the recommended three months of import, an equivalent of $750 million (about K1.3 trillion).

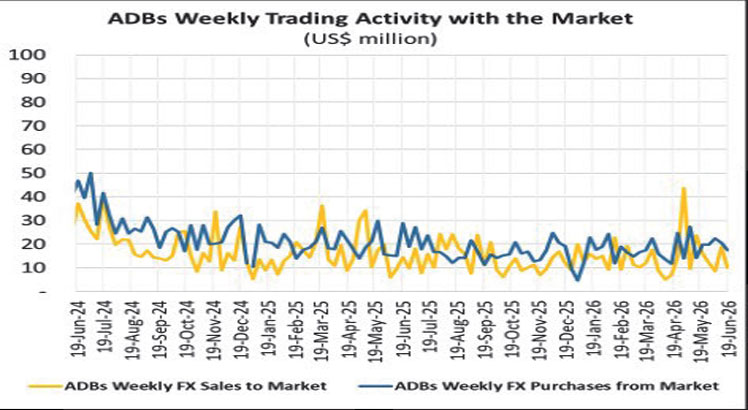

During the review period, RBM implemented several market interventions to avert the balance of payments crisis Malawi has been experiencing.

Reserve Bank of Malawi (RBM) spokesperson Boston Maliketi Banda, in an interview on Sunday, said the reforms have helped to improve price discovery and the allocation of foreign currency, creating conditions that support external sector adjustment.

He said continued improvements will depend on increasing the country’s foreign exchange earnings through higher exports, tourism, investment inflows and productivity, adding that the reforms should be seen as an enabler rather than a complete solution.

Said Banda: “While the recent improvement in reserve growth trends may suggest that some stabilisation measures are beginning to have a positive effect, the continued pressure on gross international reserves and low import cover indicate that significant challenges remain.”

In August last year, the RBM announced a reduction in the mandatory conversion rate for export revenues from 30 percent to 25 percent, with further reductions for qualifying companies anticipated.

In March last year, RBM also amended foreign exchange controls to promote import substitution and incentivise the export sector while curbing the use of informal sources of funds for importation.

RBM also reduced the mandatory conversion ratio from 70 percent to 50 percent for non-governmental organisations and introduced a verification requirement for importers to demonstrate that their imports have been financed through the formal banking channel.

Malawi Confederation of Chambers of Commerce and Industry chief executive officer Daisy Kambalame, in an interview, agreed that the reforms have moved the economy in the right direction, but described the progress as “very insignificant” as businesses are still struggling to access foreign currency.

“Without expanding the country’s capacity to generate foreign exchange, reserves accumulation and long-term stability will remain constrained despite ongoing reforms,” she said.

In its Malawi Economic Monitor, the World Bank said distortions related to RBM foreign exchange operations had affected the central bank’s balance sheet, requiring fiscal transfers and recapitalisation through the issuance of promissory notes.

The data further show that over the past five years, RBM has sold over $3.1 billion (about K5.4 trillion) in foreign exchange to the market and has purchased $2.56 billion (about K4.4 trillion), resulting in net sales of $600 million (about K1 trillion).