Limited access to affordable credit remains one of the greatest obstacles for entrepreneurs in Malawi, compelling many to depend on personal savings and informal networks to launch and sustain their businesses.

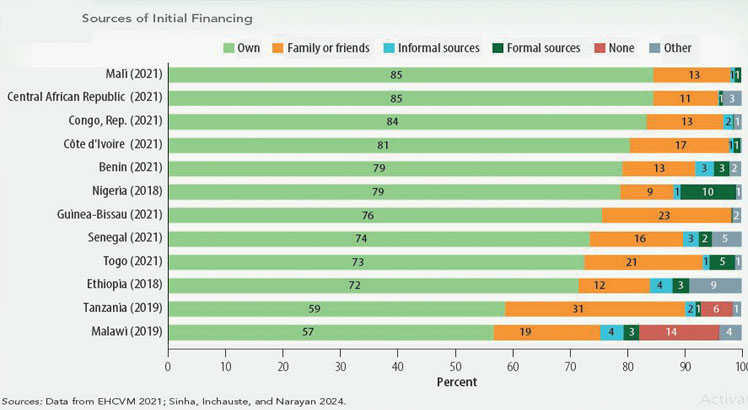

Data published in the World Bank’s April 2026 Africa Economic Update show that about 76 percent of own-account workers and non-farm household enterprises in Malawi finance their start-up capital through personal savings or support from family and friends, while only seven percent use external finance.

The report says this limited use of formal and informal credit reflects “pervasive challenges in credit markets,” which continue to constrain enterprise growth across the country.

It further notes that many small business operators prefer borrowing from social networks because “transaction costs are lower and repayment is more easily enforced through personal relationships”.

Joyce Mwanza, a cross border trader, said in an interview on Tuesday that despite having a ready market for her goods, she found it difficult to access formal credit as she did not have collateral to secure her loans.

“I ended up borrowing from my relations, but the money was not enough to grow my business as I had desired,” she said.

In a written response on Tuesday, Mzuzu University economics lecturer Christopher Mbukwa observed that Malawi’s lending rates, ranging between 25 and 37 percent and among the highest in the region, are not only a deterrent, but also suppress enterprise growth.

He said: “Most enterprises find these loans expensive and uncertain. The repayment periods are oftentimes considered too short and to get the formal loans, businesses are required to meet strict requirements.”

Former corporate banker and

investor Benedict Nkhoma said at current interest rate levels, borrowing often erodes already thin margins, making informal financing through savings and social networks the more rational choice.

He, however, warned that reliance on informal financing limits business expansion and keeps many enterprises operating at a small-scale and outside formal systems.

Said Nkhoma: “Addressing this requires not just lower rates, but broader reforms to reduce risk and improve access to affordable, structured finance including sustaining macro-economic stability which is key low inflation and easing interest rates over time.

“Strengthening credit infrastructure, expanding credit guarantee schemes and blended finance structures and promoting cashflow-based and digital lending models can also help.”

On his part, Scotland-based Malawian economist Velli Nyirongo observed that the structure and cost of finance are key barriers, noting that when 76 percent of own-account workers depend on personal savings or informal support, this indicates that formal borrowing is either inaccessible or unattractive.

He said that high interest rates, coupled with fees, collateral requirements and complex procedures,

raise the effective cost of borrowing and exclude many potential entrepreneurs.

Economist Mi lward Tobias observed that most own-account workers are excluded from bank loans because they cannot meet collateral requirements, while microfinance and group lending systems are also strained by weak repayment discipline, mistrust and political interference in some government-backed schemes.

He said that although commercial banks have recently reduced lending rates to about 20.8 percent, broader economic challenges and business fragility continue to limit loan uptake and repayment capacity.

In recent months , commercial banks have been reducing their lending rates following policy rate adjustment by the Reserve Bank of Malawi (RBM), a development analysts argued is not significant enough to transform the investment climate.

Cumulatively, commercial banks have cut lending rates by 4.4 percentage points since February from 25.2 percent to 24.7 percent before dropping twice in March to 23.7 percent and 22.4 percent after the RBM cut policy rate from 26 percent to 24 percent.

Banker s Associat ion of Malawi president Phillip Madinga is quoted as having said banks want to make loans competitive while maintaining its sustainability will depend on inflation direction.

Madinga, who is Standard Bank Malawi plc chief executive, said commercial banks can price loans more competitively while still maintaining prudent risk management.

The annual growth rate of private sector credit slightly decelerated to 44.7 percent in the fourth quarter (Q4) of 2025 from 45 percent in Q3 of the same year, but was higher than 29.4 percent registered in Q4 of 2024.

However, on a quarterly basis, the stock of private sector credit increased by K55.4 billion to K2.3 trillion during the quarter under review