Malawi’s non-performing loan (NPL) levels continue to rise, exceeding the five percent regulatory threshold, signalling growing financial stress and increased credit risk, analysts have said.

Published data from African Development Bank (AfDB) Group shows that NPLs or bad loans that are either overdue or unlikely to be repaid by the borrower, rose to nine percent in October 2024 from 6.7 percent a year earlier, exceeding the five percent regulatory threshold ratio.

Chamber for Small and Medium Enterprises executive secretary James Chiutsi said in an interview on Thursday that the going has been tough for small businesses, “even suicidal to some”.

“The environment has led to incomes being negatively affected and most businesses failing to expand and other closing shop,” he said.

In an interview on Thursday, a small-scale business operator Fletcher Luhanga, who owns a fast-food outlet in Blantyre, said plans to expand his business have halted, saying he is failing to service a K5 million loan he took from a local bank.

He said with prices of food rising every day, it has become difficult to plan as capital continues to shrink while customers are opting for home-made meals to cut on expenditure.

“There is not even a profit left, all the money is gone and I can’t service my debt anymore,” he said.

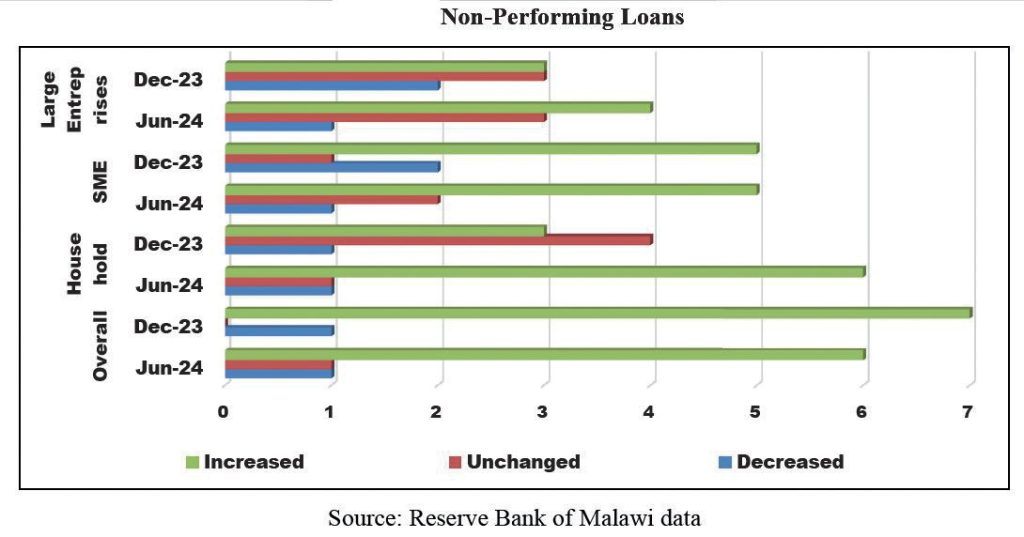

Luhanga is among small-scale business operators, including households and large enterprises that a recent Reserve Bank of Malawi Bank Lending Survey found to be struggling to meet their loan obligations.

The survey cited deteriorating macroeconomic conditions marked by rising inflation rate currently at 29.2 percent and high interest rates as well as foreign exchange shortages, which have hindered borrowers’ ability to meet their loan obligations.

Banking and financial consultant Misheck Esau said in an interview the situation is not surprising, adding that the economic environment has become challenging for many borrowers who have been in a high interest rate trap since 2021.

He said: “This has been compounded by the scarcity of foreign currency for those that depend on imports. Additionally in general, there has been a huge price spiral on the back of the foreign currency parallel market exchange rates.

“It is, therefore, not surprising, though of great concern, that non-performing loan levels are rising again. Clearly, the road to economic recovery and stability will be long and tough.”

One of the country’s financial analysts who spoke on anonymity said the rise in NPLs calls for urgent macroeconomic stabilisation and targeted support to vulnerable sectors.

“It signals rising credit risk for banks, which may tighten lending and slow down private sector growth,” he said.

Economist Bond Mtembezeka said the rise is not surprising, observing that “the economy is not in a good shape, inflation is eroding real incomes of both consumers and businesses and this translates to poor loan servicing by both”.

On his part, Scotland-based Malawian economist Velli Nyirongo observed that for the wider economy, a high and rising NPL ratio is a warning sign of underlying economic weakness.

An analysis of the banks’ financial statements shows that a large chunk of the NPLs come from personal loans, agriculture, manufacturing, retail and construction as well as electricity, water and energy sectors.

Meanwhile, RBM data shows that annual growth rate of private sector credit decelerated to 17.8 percent in March 2025 from 19.7 percent in February 2025 and was lower than the 26.6 percent recorded in March 2024.

On a month-on-month basis, private sector credit increased by K1.2 billion to K1.5 trillion in the review month, primarily driven by increases in individual household loans and mortgages, according to the RBM.