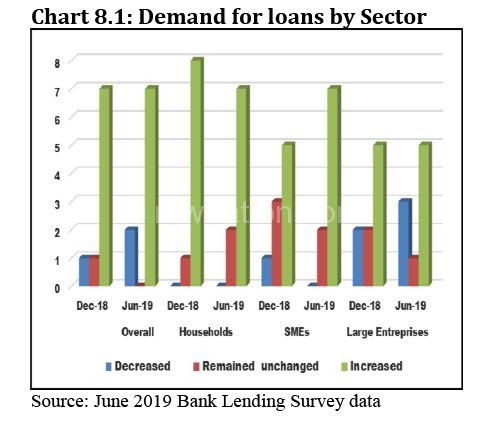

The banking sector’s demand for loans and credit lines have increased amid declining bad loans, the Reserve Bank of Malawi (RBM) has said.

According to the RBM’s Bank Lending Survey (BLS), covering a six-month period from January to June 2019 in nine commercial banks, the increase in demand for loans and credit lines mainly emanated from the household and small and medium enterprises (SMEs) sectors.

With regard to large enterprises, however, BLS found that the general perception by banks was that credit growth had slowed down during the surveyed period largely due to seasonal factors and uncertainty surrounding the general elections.

Contrary to the previous survey results where loans were reported to be more of short-term, majority of banks during the June 2019 survey period reported an increase in both short-term and long-term loans, implying increased confidence in the market.

The banks’ perceptions somewhat reflected the actual credit developments as private sector credit strongly expanded by 9.8 percent (K45.0 billion) between January and June 2019 compared to a growth of 6.6 percent (K28.4 billion) during the previous survey period and 4.5 percent (K18.5 billion) registered in corresponding survey period in 2018.

“The increase in the demand for loans by households was mainly due to increases in consumption expenditure, improved consumer confidence and drop in interest rates that made borrowing relatively cheaper. With regard to large enterprises, however, banks indicated that most of their existing clients did not extend their credit lines and at the same time there was a general slowdown in demand for credit from new customers,” reads the report in part.

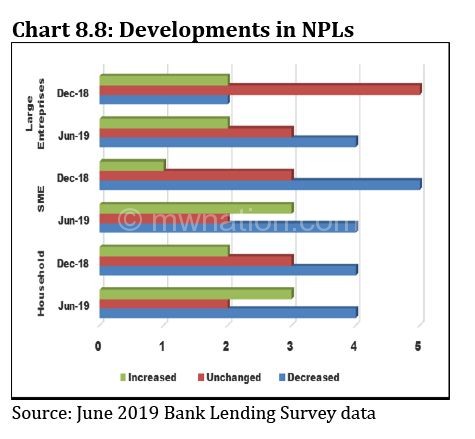

Meanwhile, the during the period under review, there was a general decrease in non-performing loans (NPLs) in all the three economic agents during the past six months to June 2019, similar to the December 2018 survey results.

This is consistent with actual data, which shows that the level of NPLs decreased to K27.5 billion in the surveyed period from K31.4 billion during the preceding survey period and K61.6 billion in a corresponding survey period in 2018.

According to the report, the levels of NPLs in the wholesale and retail sector were highest at K12 billion, seconded by the agriculture sector at K3.6 billion and manufacturing sector at K2.4 billion.

This is in contrast to the December 2018 survey findings where most banks ranked the Manufacturing sector as the sector with highest levels of NPLs followed by the Transportation sector. Community, Social and Personal services and Construction sectors were ranked third.

“Most banks largely attributed the decrease in NPLs to write-offs. Nonetheless, enhanced credit monitoring, improved loan recovery efforts and decline in lending rates that enhanced loan repayment capabilities by the borrowers also contributed to the sustained decline in NPLs.”

RBM Governor Dalitso Kabambe earlier said the central bank is targeting to reduce levels of NPLs to five percent, which is the minimum regulatory requirement, on the back of improved macroeconomic environment.

Money market analysts say the high NPL ratio is indicative of the difficult economic situation, with borrowers often failing to generate sufficient returns from their businesses to repay their loans.

The National Working Group on Trade Policy chairperson Frederick Changaya said earlier that the group is banking on reduced levels of bad loans for softer default risk premiums, adding that with high NPLs, companies are paying high default risk premiums—the difference between a debt instrument’s interest rate and the risk-free rate.