Economist Intelligence Unit (EIU) says the persisting Covid-19 pandemic, depreciating exchange rate and inflationary pressures pose risks to accommodative monetary policy in the short to medium-term.

In a brief contained in the November 2021 Nico Asset Managers Monthly Economic Report, EIU said it sees no further easing of the policy rate as inflation rate remains above the Reserve Bank of Malawi (RBM) target of plus or minus five percent coupled with the depreciating exchange rate.

EIU, the research and analysis division of the Economist Group of United Kingdom, sees the RBM adopting a tightening stance from this year as inflationary pressures build on the back of rising global oil prices and improved consumer sentiment.

Reads the report in part: “Given inflation pressures, there is little hope for further easing of Malawi’s policy rate even if the domestic demand remains weak.”

If the RBM adopts a tight monetary policy, it means reducing money supply and increasing the policy rate, currently at 12 percent, which could trigger a rise in interest rates. In contrast, accommodative or loose monetary policy generally includes lowering interest rates.

The Malawi Confederation of Chambers of Commerce and Industry (MCCCI) has also projected that pandemic-induced supply-demand mismatches, which triggered a rise in inflation in 2021, could force RBM to implement contractionary or tight monetary policy to counter the rise in inflation rate currently at 11.1 percent.

“The RBM could reduce money supply or increase interest rates which could prematurely bring to a halt monetary support towards the recovery of the economy,” reads MCCCI’s 2021 Assessment of Business Environment.

In an interview on Wednesday, Malawi University of Business and Applied Sciences associate professor of economics Betchani Tchereni said contractionary monetary policy rate stance is inevitable which could result in hiking policy rate.

He said: “Where we stand, we have such a huge demand for imports which is likely to push the depreciation of the kwacha further, causing imported inflation.

“As such, it is only prudent to control the supply of money so that people’s demand for imports is controlled.”

Tchereni, however, said the solution to the country’s challenges is not tightening monetary policy, but industrialisation.

“It is high time we industrialised as a country so that the import demand push inflation can be controlled. Otherwise the five percent target is a far-fetched idea, especially where data misreporting can no longer be entertained,” he said.

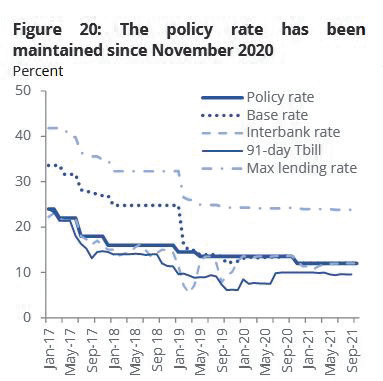

The policy rate has been declining since November 2016 and was stable at 13.5 percent for the most part of 2020 before being revised downwards to 12 percent in November 2020.

In the last Monetary Policy Committee (MPC) meeting, the RBM also maintained the policy rate at 12 percent, stabilising lending rates in commercial banks at the current average of 12 percent.

RBM also revised its projection for annual average headline inflation rate for 2021 from 8.4 percent during the third MPC meeting to 9.1 percent during the fourth MPC meeting, reflecting the impact of hikes in commodity prices.

On the other hand, the local currency keeps losing value against major trading currencies.

In the just-ended year, the kwacha retreated from an average of K778 in January to K823 as at December 2021.