VILIPO MUCHINA

MUNTHALI*

Contributor

This article is the second part of a detailed exploration of intra-group services in transfer pricing.

While the first part addressed the concept of intra-group services and determining whether services were rendered, the second part focuses on determining an arm’s length remuneration, cost allocation methodologies, the treatment of low-value-adding services, and the application of withholding taxes.

Proper pricing of intra-group services is crucial to ensuring compliance with the arm’s length principle while mitigating risks of tax disputes and double taxation.

Determination of arm’s length remuneration for intra-group services

Once it has been established that an intra-group service has been rendered, it is necessary to determine whether the fee charged is consistent with the arm’s length principle. The arm’s length principle requires that the fee should reflect what would have been agreed upon between independent enterprises in comparable circumstances.

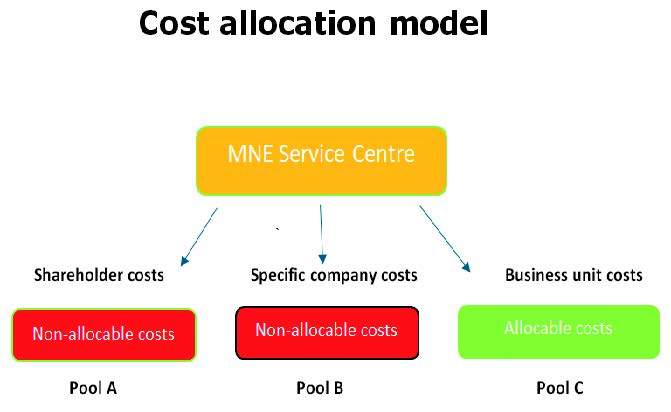

Determination of the cost base

The cost base serves as the foundation for calculating the remuneration of the service provider which often includes an appropriate mark-up. It is therefore important to identify the actual service arrangements between the associated enterprises involved in the intra-group services in order to quantify the appropriate charge for a service that has been rendered and allocate the costs incurred by the service provider appropriately among group enterprises benefiting from the services. The cost allocation must be reasonable, transparent, and aligned with the benefit test.

The direct charge and the indirect charge methods facilitate the allocation of costs incurred in the provision of intra-group services.

Direct charge method

This method is applied in circumstances where services rendered can be specifically identified, quantified and the associated costs directly linked to specific group enterprises. For example, legal services provided to resolve a specific subsidiary’s litigation are allocated directly to that subsidiary.

However, the direct charge method is often difficult to apply in practice as it is an administrative burden which is disproportionate to the services provided.

Indirect charge approach

If a direct charge method is difficult to apply, the multinational enterprise (MNE) group may apply the indirect charge method whereby the charges for services rendered are determined by allocating the costs across all potential beneficiaries. In determining the costs to be allocated, both direct and indirect costs are considered to derive total costs which are subsequently allocated to service recipients based on an appropriate allocation key.

The choice of the allocation keys is based on an appropriate measure of the usage of the service that is also easy to verify. The commonly used allocation keys include net sales of the service recipient as a proportion of the total sales of the group; time spent by employees performing an intra-group service; units issued, produced, or sold; headcount; space used; payroll; asset size or a combination of cost allocation keys.

Inclusion of a profit element

Independent service providers typically charge a profit mark-up above their costs to earn a return on their investment and compensate for the risks associated with providing the services. Similarly, to ensure compliance with the arm’s length principle, a profit mark-up must be included in the charges for intra-group services.

Selecting an appropriate transfer pricing method

The arm’s length remuneration of an intra-group service is determined by applying the most appropriate method to the circumstances of the case. The transfer pricing methods which are often applied to determine an arm’s-length transfer price for intra-group services include the comparable uncontrolled price (CUP) method and cost-based methods (cost plus method or transactional net margin method).

The CUP method

The CUP method is applicable when specific services that form the core business activity of the enterprise are provided not only to associated enterprises, but also to independent enterprises. The amount charged in such circumstances is determined in the same way as charges to independent enterprises.

The cost-based methods

The cost-plus method and the transactional net margin method test the arm’s-length nature of the intra-group service fees by reference to gross profit mark-up and net profit margin respectively realised in a comparable uncontrolled transaction.

The cost-based methods would likely be most appropriate in the absence of a CUP but where the nature of the activities involved, assets used, and risks assumed are comparable to those undertaken by independent enterprises.

Low-value adding Intra-group services

The low-value-adding services are routine or supportive in nature; are not part of the core business of the MNE group; do not require use of unique and valuable intangibles; do not involve assumption of significant risks and do not significantly contribute to the MNE’s value creation. These services include informaton technology support, payroll processing, routine accounting, legal and general or administrative services.

Irrespective of the categories of services, in determining the arm’s length charge for low value-adding intra-group services, the Organisation for Economic Cooperation and Development (OECD) recommends the application of a simplified approach whereby a fixed mark-up of five percent (on chargeable costs) is deemed arm’s length and does not need to be justified by further benchmarking studies.

The simplified approach reduces the administrative burden as it requires less detailed documentation and provides greater certainty for MNE groups that the intra-group pricing for the qualifying activities will be accepted by the tax authorities.

However, the domestic law in Malawi has not adopted this approach. The simplified fixed mark-up of five per cent can be challenged by the tax authorities as it is not supported by the domestic law. Therefore, taxpayers are required to conduct robust benchmarking studies to justify the pricing for such services.

Withholding taxes on intra-group services

Intra-group services often trigger withholding tax obligations in the jurisdiction of the service recipient if the service payments are classified as taxable under domestic law or the payment is not exempt under an applicable double taxation agreement.

The levying of withholding taxes on the provision of intra-group services can prevent the service provider recovering the totality of the costs incurred for rendering the services. When a profit element or mark-up is included in the charge of the services, WHT applies only to the amount of the profit element or mark-up.

Conclusion

Intra-group services represent a significant area of transfer pricing due to their prevalence and complexity. By carefully determining arm’s length charges, implementing robust cost allocation methodologies, appropriately handling low-value-adding services, and ensuring compliance with withholding tax obligations, MNEs can mitigate risks and enhance compliance.

The next article in this series will delve into financial arrangements and their transfer pricing implications. Stay tuned!

*Vilipo Muchina Munthali is managing Consultant at Swift Resources, an international tax and transfer pricing consulting firm that specialises in developing, implementing and defending transfer pricing policies

Feedback: vilipo@swiftmalawi.com